Quant Research

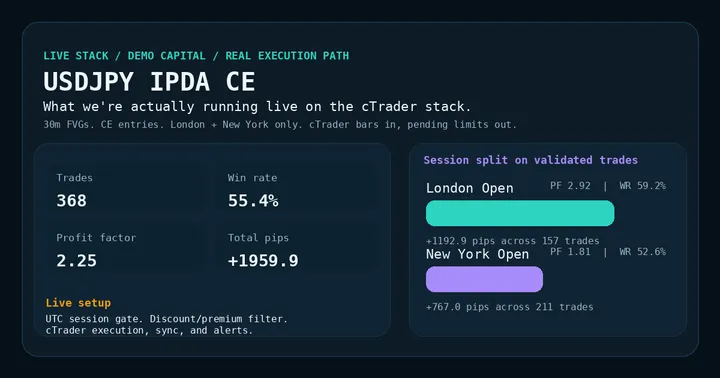

What We're Actually Running Live: USDJPY IPDA CE on cTrader

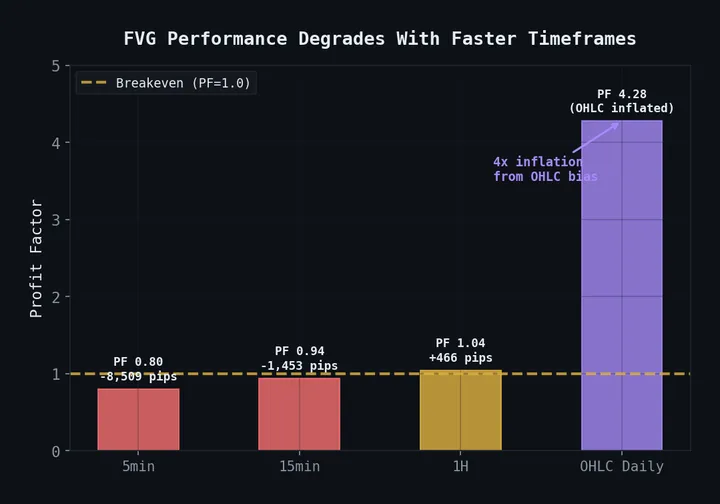

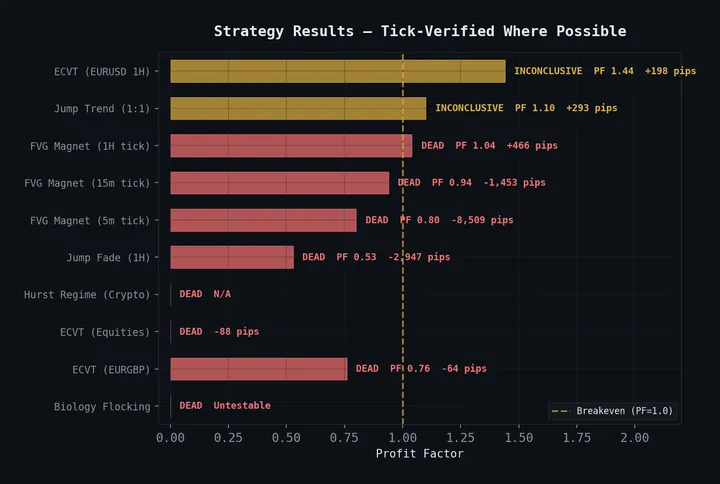

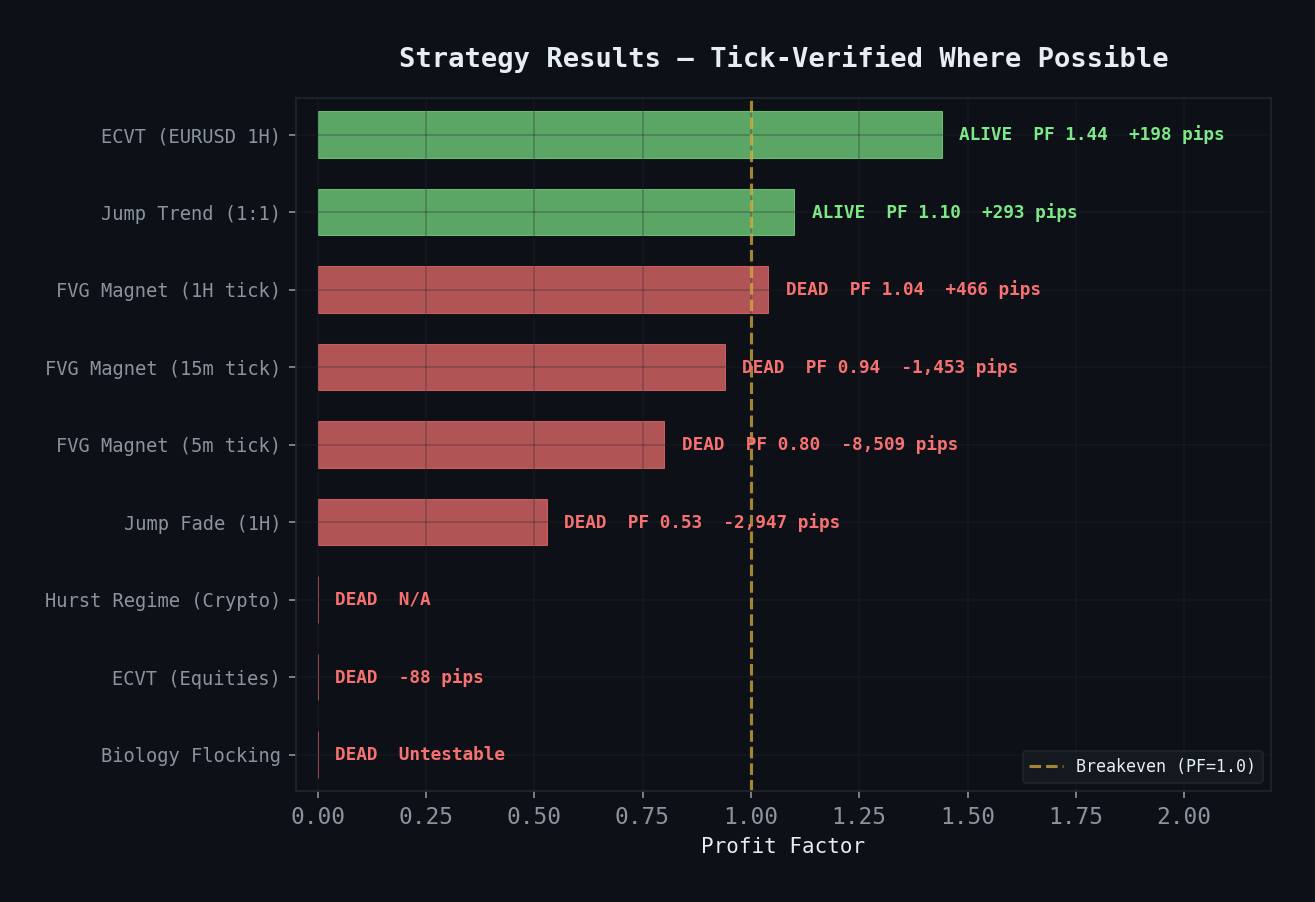

After killing a graveyard of ideas, this is the one we kept: a 30-minute fair value gap strategy on USDJPY, executed through cTrader with real order plumbing, session gates in UTC, Discord alerts, and enough operational paranoia to survive reboots and outages.